Traditional lending is the realm of regulated banks and financial institutions that offer loans to creditworthy individuals. In contrast, crypto lending is still widely unregulated and offers opportunities and risks for lenders and borrowers.

- What is traditional lending?

- Pros and cons of traditional lending

- What is crypto lending?

- Pros and cons of crypto lending

- Comparison of traditional lending and crypto lending

What is traditional lending?

In the traditional banking system, fiat loans are obtained from a bank or regulated financial institution through a complex loan approval process that requires application forms and creditworthiness proven by a credit check. A borrower must achieve a certain rating in the credit scoring process that takes into account their prior lending and payment history. If a borrower is classified as a credit risk, they won’t be able to access loans with the best interest rates and might not be able to borrow at all.

Larger fiat loans usually need to be secured with collateral, such as a car, home or other valuable conventional asset. These products are known as collateralized loans. If a borrower defaults on the loan, the physical asset will be seized or repossessed.

Pros and cons of traditional lending

Traditional lenders are subject to stringent banking regulations. Their interest rates are based on those set by central banks or federal reserves that commit to maintaining a target interest rate. When a central bank or reserve raises rates, lending banks will follow, and vice versa.

Competition between banks, demand for loans, or a borrower’s creditworthiness can also influence interest rates. This all means that any conventional loan interest rate comparison will show little rate deviation between lenders and higher rates for lower credit scores. Traditional lending isn’t a free market, and borrowers with a poor credit history or lack of credit history can be excluded.

The positive side of traditional lending, however, is that heavy regulation offers defined processes and a level of consumer protection should something go wrong. For instance, it’s virtually impossible for an illicit actor to become a major or mainstream loan provider, and all traditional lenders must balance their own interests with those of the consumer.

What is crypto lending?

In cryptocurrency lending, borrowers can use their cryptocurrency assets as collateral to obtain a crypto or fiat loan. Crypto owners or lenders can also enter into specific agreements with borrowers, facilitated by lending platforms.

Cryptocurrency owners can also become lenders on peer-to-peer (P2P) lending platforms by adding their assets to a liquidity pool or decentralized finance (DeFi) protocol acting as a lending platform for borrowers.

Crypto lending platforms usually facilitate loans between lenders and borrowers, providing the infrastructure for lenders and borrowers to transact through smart contracts and blockchain technology where loan terms can be verified and transactions occur autonomously.

There are two main types of crypto lending: centralized and decentralized crypto lending.

- Centralized crypto lending

Centralized crypto lending platforms are operated by a single entity or business that acts as an intermediary between lenders and borrowers and will charge fees. Lenders can earn interest, and borrowers will pay interest and usually need to provide collateral in the form of their crypto assets. Smart contracts are used to verify transactions and ensure that loan terms are met. If a borrower defaults on a loan, the lender will receive the agreed collateral.

- Decentralized crypto lending

Decentralized or P2P lending platforms are DeFi protocols where lending is completely automated with the help of smart contracts. These platforms can have lending pools where cryptocurrency owners commit their assets as liquidity for lending in return for rewards and/or interest. Smart contracts distribute or collect loans based on set criteria, and interest rates can be determined by an algorithm.

Pros and cons of crypto lending

There are no credit checks or application forms in crypto lending, and transactions can be processed in minutes without the lengthy application and approval process found in traditional banking. Crypto lenders and borrowers usually only need to register with a platform, provide identity verification, and connect their cryptocurrency wallets.

Interest rates and terms, as well as any rewards, are set by crypto lending entities and the market. The rate of return for crypto lending can be higher than the interest rates offered by traditional banks on conventional savings products. Cryptocurrency lending allows investors to earn a return on their crypto assets.

The major downside of inherently risky crypto lending, however, is that a lack of regulation results in zero protection for lenders or borrowers, and illicit actors in the sector are rife.

Crypto price volatility also means collateral or liquidity committed by borrowers or lenders can quickly decline in value. Falling collateral value increases a lender’s risk if a borrower defaults and can affect a borrower’s ability to repay a loan.

In addition, lending platforms may liquidate a loan if price volatility means it fails to meet the required loan-to-value (LTV) ratio. The LTV ratio is a financial metric used to measure the amount of a loan compared to the value of the asset securing the loan.

Although blockchain technology provides security and speed for crypto loan transactions, there is also a risk that smart contracts will have vulnerabilities or bugs, particularly in DeFi protocols, that will leave them exposed to attackers.

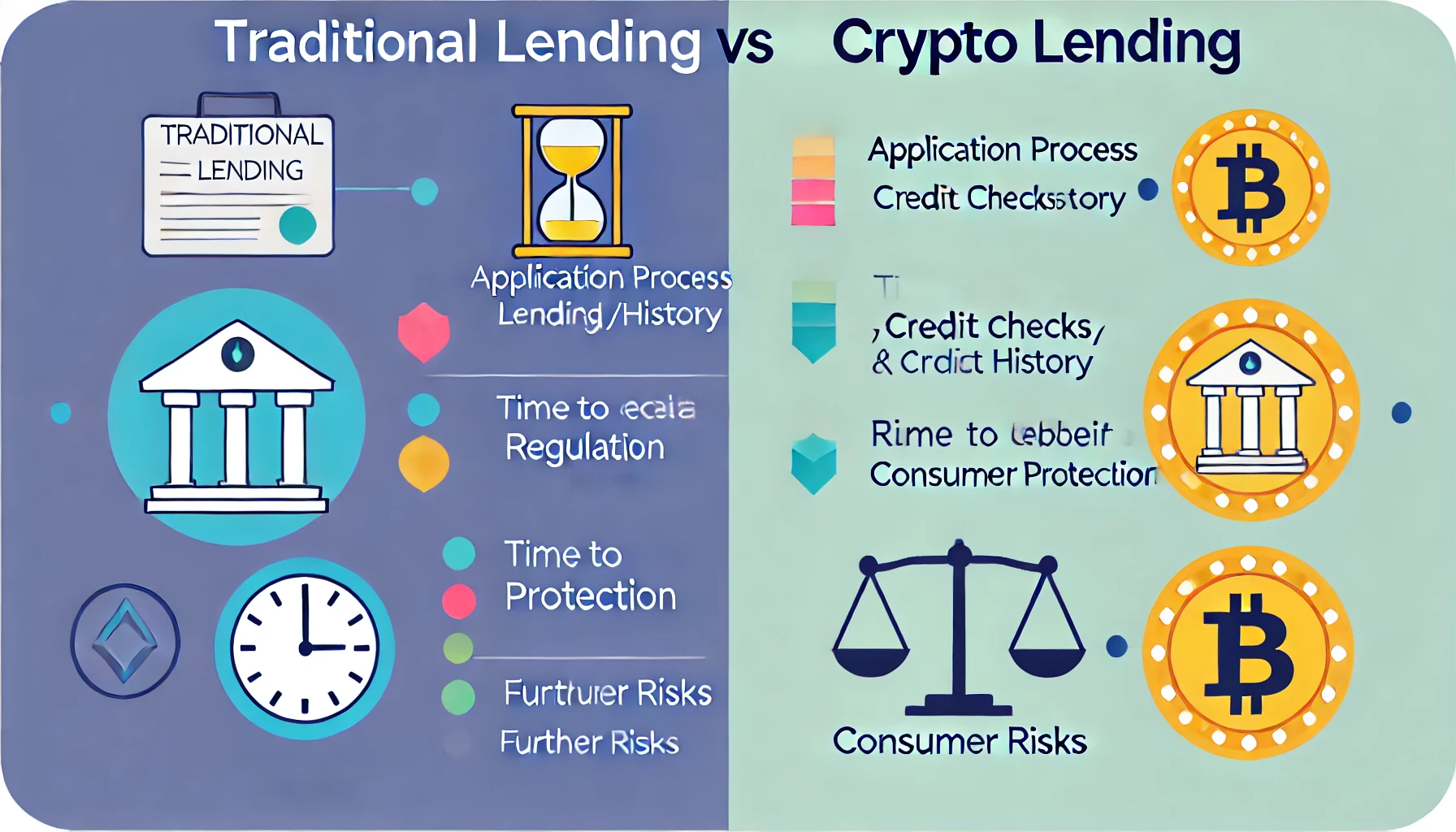

Comparison of traditional lending and crypto lending

The key differences between traditional and crypto lending are explained below:

| Aspect | Traditional Lending | Crypto Lending |

|---|---|---|

| Application process | Lengthy loan approval process with application forms | Register and provide ID |

| Credit checks/history | Credit history and credit score | None |

| Time to obtain a loan | Days/weeks | Minutes |

| Regulation | Heavily regulated | Unregulated |

| Consumer protection | Available | None |

| Further risks | Loans may be denied, missed payments or defaults lead to repossession and affect creditworthiness | Crypto price volatility, loan defaults, illicit actors, smart contract vulnerabilities, and future regulations |

Crypto lending gained popularity when the COVID-19 pandemic negatively impacted the returns on traditional investment products such as savings. It also emerged as a way for cryptocurrency owners to put their assets to work while retaining ownership.

For borrowers, crypto lending allows the use of these digital assets as collateral and negates the need for a credit history or any creditworthiness. Crypto lending is another sector that serves the world’s unbanked and provides near-instantaneous transactions.

However, despite the benefits and potentially high returns, the crypto lending sector has its own risks and shares the risks associated with cryptocurrency use, such as price volatility, illicit actors, and technological vulnerabilities. Evolving global cryptocurrency regulation has the potential to add restrictions to the crypto lending sector in the future. Some countries have already prohibited cryptocurrency lending.

Due to heavy regulation and consumer protection, traditional loans are harder for borrowers to obtain but much safer. Furthermore, individual asset owners cannot simply become lenders to earn a return on their assets.