Pave Bank — a licensed commercial bank from Georgia that unites fiat and digital assets within a single regulated framework. Its architecture is based on the principles of programmable banking and integration with blockchain networks for transparent and instant settlements. In 2025, the bank raised $39 million from Accel, Tether Investments, and Wintermute to scale its technology and expand its global presence. Through the PaveNet network, multi-asset accounts, and tokenization tools, Pave Bank transforms into an infrastructure where money and code operate as one system. The project demonstrates how blockchain can be used not as an alternative to the banking system, but as a technological layer built upon it.

- Pave Bank — license, mission, and market niche

- Programmable banking and the role of blockchain

- Multi-asset accounts, PaveNet, and asset tokenization

- Security, blockchain transparency, and compliance

- Funding, growth strategy, and blockchain integrations

Pave Bank — license, mission, and market niche

Pave Bank is registered as JSC Pave Bank Georgia and obtained banking license No. 305 from the National Bank of Georgia in December 2023. From the very beginning, the bank focused on combining traditional finance and digital assets in compliance with existing regulations. Its mission is to create a “bridge” between the banking system and the blockchain economy, providing access to tokenized assets and secure on-chain operations. Pave aims to prove that digital assets can exist under regulatory supervision without losing efficiency.

Blockchain in Pave Bank’s model is not a replacement for accounting — it acts as a technological layer for transparency and settlement. Through blockchain networks, the bank records operations, verifies asset origins, and ensures data immutability. This blend of open technology and banking compliance forms the basis of a new type of financial service — regulated blockchain banking, where every transaction is both controlled and verifiable.

Programmable banking and the role of blockchain

The core idea of Pave Bank is programmable banking — the ability to write “code on top of money.” Clients can create logical scenarios where payments and settlements occur automatically under specific conditions. This concept is built on smart contracts adapted to banking-grade security standards. Unlike open DeFi platforms, Pave employs private, permissioned blockchain networks to maintain full control over data and ensure compliance with KYC/AML requirements.

-

Smart contracts for business processes — automate settlements between parties via predefined logic.

-

On-chain identity — corporate clients can verify their status using tokenized identifiers.

-

Integration with external blockchains — transactions and reserves can be mirrored in public networks for data verification.

Thus, blockchain becomes the foundation for payment automation and trust among participants. It gives banking operations transparency and immutability, turning every action into a verifiable event rather than just a database entry.

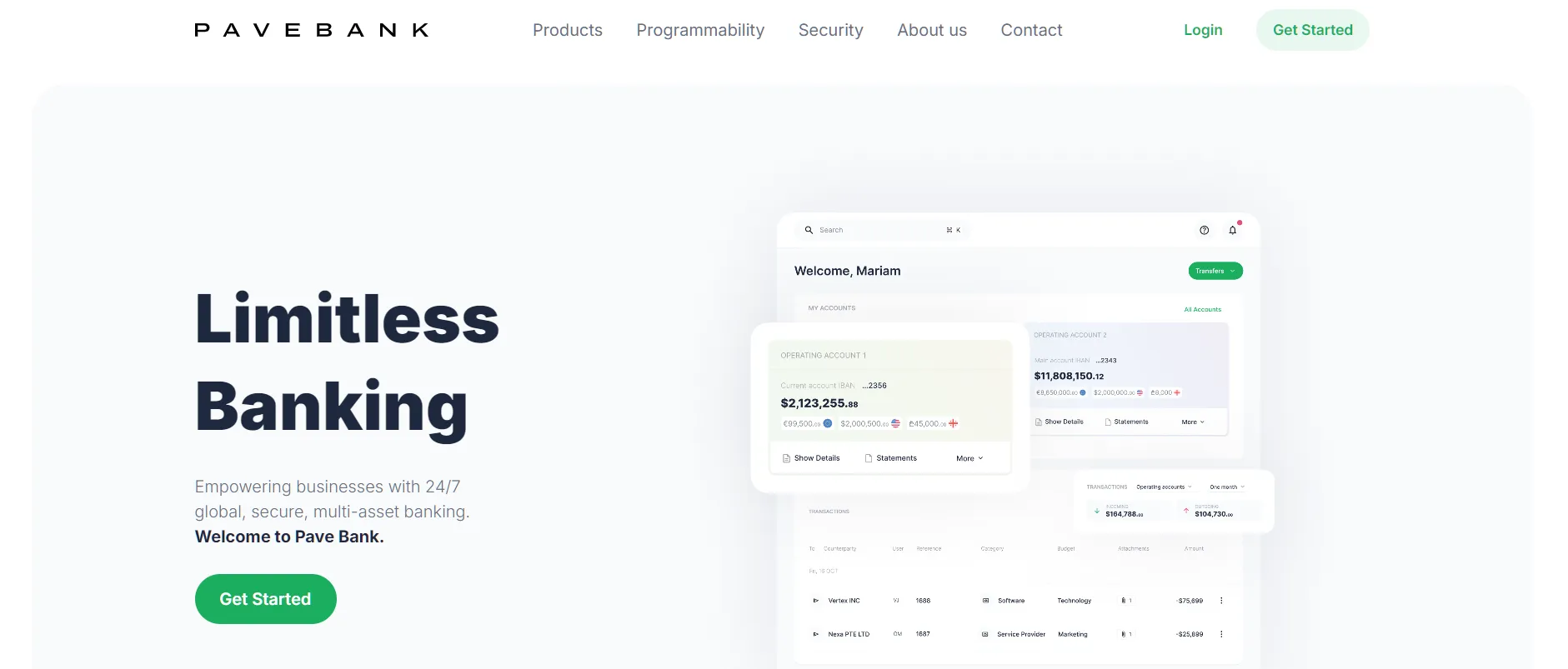

Multi-asset accounts, PaveNet, and asset tokenization

Pave Bank has built a product ecosystem where fiat, stablecoins, and digital assets are managed through a unified interface. The PaveNet network, designed on blockchain payment channel principles, enables 24/7 instant transactions and on-chain accounting within corporate networks. Clients have access to OTC tools, asset conversions, and programmable money flows.

| Component | Capabilities | Client Value |

|---|---|---|

| Multi-asset accounts | Support for fiat, stablecoins, and tokenized assets | Centralized liquidity management |

| PaveNet | Blockchain network for instant settlements | Transparent operations and reduced fees |

| Asset tokenization | Creation of digital equivalents of fiat and real-world assets | Expanded liquidity and new business models |

| Smart trading and OTC | Automated deals with on-chain verification | Reduced risk and fewer manual errors |

The use of blockchain enables Pave to launch new products, such as tokenized debt instruments, corporate stablecoins, and digital promissory notes. This makes the bank attractive not only to traditional companies but also to Web3 projects seeking a regulated entry point into the banking ecosystem. In the long run, PaveNet may become part of an interbank instant settlement network, where blockchain ensures trust without intermediaries.

Security, blockchain transparency, and compliance

The Pave Bank model is based on a full reserve approach — every asset is backed by real funds and reflected on the blockchain. This eliminates credit risk and builds client confidence. Compliance is handled via smart contracts that automatically monitor limits, jurisdictions, and fund origins. All operations can be recorded in private blockchain ledgers accessible to auditors and regulators.

The application of blockchain technology enhances not only security but also transparency in internal reporting. Institutional clients can receive on-chain proof of reserves and transaction statuses. This reduces counterparty risk and prevents manipulation of financial records. In this way, blockchain serves not merely as a technology but as a next-generation compliance instrument embedded directly into the banking architecture.

Funding, growth strategy, and blockchain integrations

In October 2025, Pave Bank raised $39 million from leading investors, including Accel, Tether Investments, and Wintermute. The funds are aimed at expanding international licensing, scaling the PaveNet network, and deploying blockchain-based solutions for corporate clients. The company plans to launch APIs for direct integration with Web3 applications and support cross-chain interaction with networks such as Ethereum, Polygon, and Stellar.

In the future, Pave is considering issuing tokenized deposits and corporate lending instruments on the blockchain. This will create the foundation for “programmable assets,” where liquidity is managed by code and settlements occur instantly and transparently. Thus, Pave Bank is taking the next step from neo-banking to blockchain-native banking, forming a new class of financial institutions in which decentralized technology and traditional oversight work in full harmony.